Who Gets Paid When a Machine Makes Art: The Business of AI Creativity

The companies profiting from AI creativity are not the people who made creativity worth automating. Understanding why requires looking at the money.

There is a version of the AI and creativity story that reads like a press release.

Technology companies built powerful tools. Creative people adopted them enthusiastically. Productivity soared. Access expanded. The market rewarded innovation, and the rising tide lifted all boats. Everyone is better off. Isn’t this exciting.

That version exists. Parts of it are even true. The tools are genuinely powerful. The productivity gains are real. Some creative professionals are navigating this moment with more capability and reach than they had before.

But that version runs alongside another one that does not show up in the same TechCrunch headlines. In this version, a 3D animator who spent twelve years building the supplemental graphics that make documentary television feel like something — the animated recreations of historical battles, the visualizations of deep-sea biology, the illustrated sequences that turn an expert’s explanation into something a viewer can actually see — describes watching that entire category of work vanish. Not slowly. Not after a period of reskilling and graceful transition. Just gone, absorbed by AI tools that produce a serviceable version in minutes at a fraction of his day rate.

Both things are true simultaneously. The companies are making billions. The animators are losing their markets. And understanding how both can be true at once — how AI creativity generates record corporate revenue at the exact same moment it eliminates livelihoods built over decades — requires looking directly at the business mechanics underneath the story, rather than the version designed to be told at investor presentations.

The Numbers, Honestly

Start with scale, because the scale is genuinely staggering and understanding it helps explain why the business incentives are what they are.

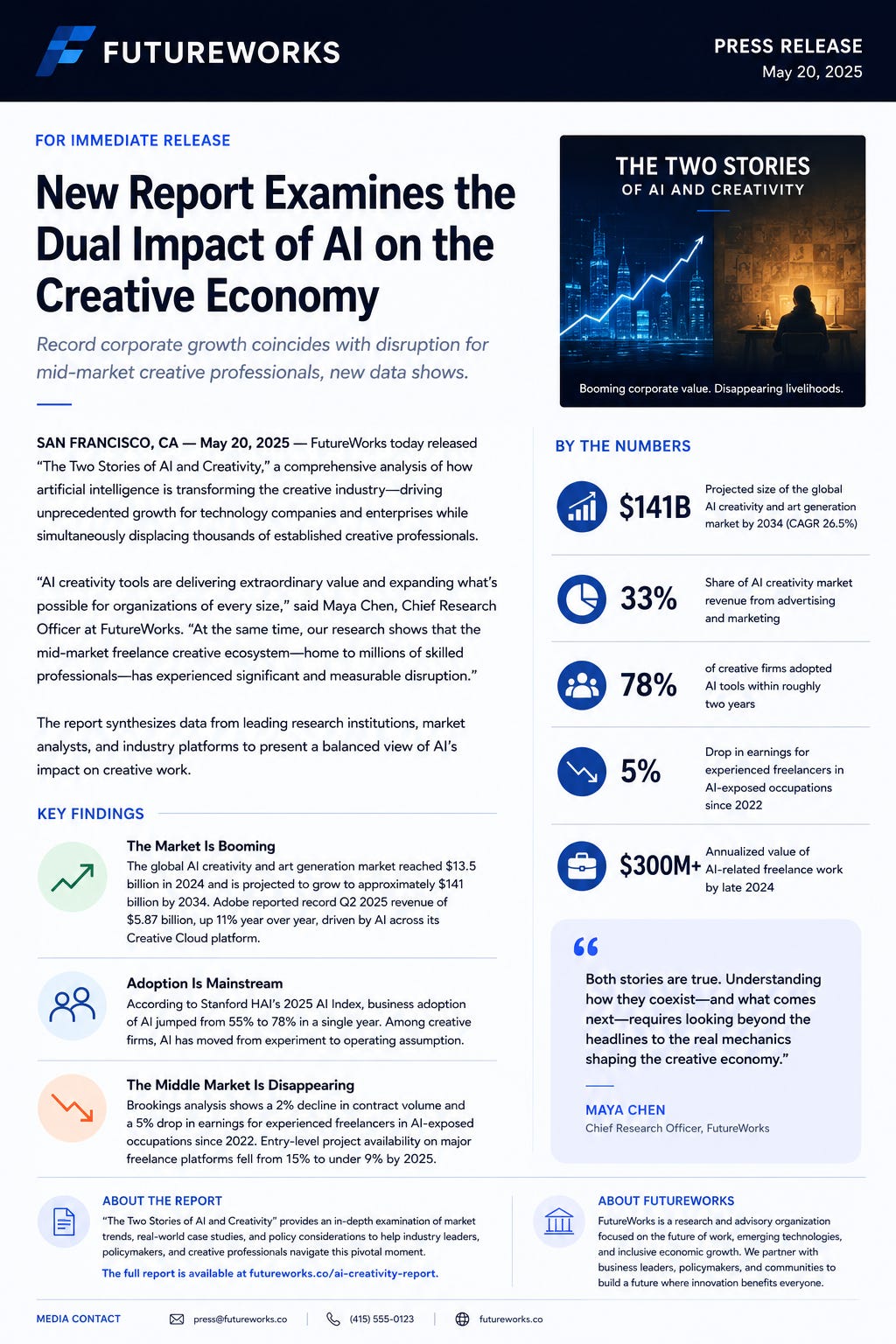

The global AI creativity and art generation market reached $13.5 billion in 2024. It is projected to grow at a compound annual rate of 26.5% for the next decade, reaching roughly $141 billion by 2034. Advertising and marketing alone account for nearly a third of current revenue, as enterprises generate personalized content at volumes and speeds no human creative team could approach.

Adobe reported record revenue of $5.87 billion in the second quarter of 2025, an 11% increase year over year, and credited the growth directly to AI integration across its Creative Cloud platform. Firefly, Acrobat AI, GenStudio — these tools generated over $125 million in AI-specific annual recurring revenue, with projections to double that figure by year end. Adobe’s stock climbed. Investors were pleased.

The Stanford HAI 2025 AI Index provides the broader frame: generative AI attracted $33.9 billion in global private investment in 2024, up 18.7% from the year before. Business adoption of AI jumped from 55% of organizations to 78% in a single year. Among creative firms specifically, that 78% figure means that within roughly two years, AI moved from an experiment to an operating assumption.

These numbers represent real value. Software that allows a small marketing team to produce visual assets at the speed of a large one, that lets a global brand localize campaigns across dozens of markets without proportionally scaling headcount, that gives a one-person design studio the output capacity of a studio three times its size — these are legitimate capabilities that solve real problems. The market is not wrong to value them.

But value created for whom, distributed to whom, and extracted from whom are entirely different questions from whether value is being created at all. And on those questions, the picture looks considerably less triumphant.

The Middle Is Gone

Something happened to the freelance creative market around 2023 that the trade publications covered gently and the financial press mostly ignored.

The middle collapsed.

Not the top. Elite creative work — the kind that commands premium rates because it requires irreplaceable judgment, distinctive vision, and a reputation built over years of visible, accountable output — has largely held. Brands still pay significant money for creative direction that carries strategic weight. Agencies still charge for thinking that goes beyond execution.

Not the bottom, either. Commodity volume work was always low-margin and remains so, now produced faster and cheaper than before.

What disappeared was everything in between: the logo commissions, the social media packages, the quick brand refreshes, the illustration work, the mid-market content writing, the motion graphics that used to require a specialist. The work that required years of genuine skill to do well but did not carry the premium of famous skill. The work that paid a graphic designer in a mid-sized city a living wage while she built her practice. The work that sustained thousands of working illustrators who were never going to be in galleries but could make a real career doing what they were good at.

A Brookings Institution analysis provides the most careful data available on this. Freelancers in occupations most exposed to generative AI experienced a 2% decline in contract volume and a 5% drop in earnings following the release of major AI tools in 2022. Those percentages sound modest until you understand who they are measuring: experienced freelancers offering higher-priced, higher-quality services. Not the beginners. The established practitioners. The ones who had worked longest and built the most — and who were most directly replaced.

Entry-level project availability on major freelance platforms fell from 15% to under 9% by 2025. More than half of the businesses that had spent money on freelance platforms in 2022 had stopped entirely by 2025. AI-related freelance work — meaning work that involves managing or directing AI systems rather than doing the creative work independently — crossed $300 million in annualized value by late 2025, with practitioners who repositioned around AI commanding rates 25 to 60% higher than those who did not.

The market did not shrink overall. It restructured. The value flowed toward people who could position themselves at the interface between human judgment and machine output, and away from people whose primary offering was the skilled execution of creative tasks that AI could now approximate. That is a brutal distinction if you spent a decade developing exactly that kind of skilled execution and built your income around it.

An Association of Illustrators survey of nearly 7,000 illustrators found that one in three had already lost work to AI, at an average cost of $12,500 in wages. This is worth sitting with. Not as a statistic. As a specific number representing a specific loss experienced by a specific person — a person who spent years learning to draw, who built a client base, who negotiated rates and managed invoices and developed a body of work, and who watched the market for that body of work contract in a period of roughly eighteen months.

What Hollywood Fought For, and What It Got

In May 2023, the Writers Guild of America went on strike. In July, SAG-AFTRA joined them. For 191 days — the longest combined stoppage in Hollywood since both unions last struck simultaneously in 1960 — American film and television production ground to a near halt. Scripts went unwritten. Productions went unfilmed. Premiere dates shifted. The economic impact ran into the billions.

The strike was about streaming residuals, which had eroded as the industry migrated from broadcast and DVD sales toward platforms that paid differently and less. But it was also, centrally, about AI. Studios wanted the ability to use AI to generate scripts, to scan actors’ faces and synthesize performances without the actor’s participation, and to train AI systems on performers’ voices and likenesses without consent and without compensation. What they were describing was a future in which the human beings who had historically been paid to create could be increasingly replaced by systems trained on their own creative output.

The WGA reached a deal in September 2023. SAG-AFTRA followed in November, with 78% of its 160,000 members ratifying the contract. The agreements were genuinely historic: the first major labor contracts in any industry to include substantive AI provisions. Studios were required to disclose AI use, obtain consent before creating digital replicas of performers, and compensate actors when their likenesses were used in AI-generated content.

The victory was real. It was also partial.

Critics — including some union members and outside legal analysts — noted that the language around generative AI was written broadly enough that studios retained significant latitude for uses that could still displace workers. The provisions around training data were especially contested: the question of whether studios could use existing recordings and performances to train AI systems was handled with language vague enough to leave the most important questions unresolved. The Center for Democracy and Technology characterized the agreement as establishing important principles while noting that the real battles lay ahead.

The deeper significance of the strike was not the specific provisions it secured. It was the precedent it established: that creative labor has a legitimate economic claim on AI systems built from that labor, that this claim can be negotiated rather than simply assumed away, and that collective action remains possible even in industries where the power differential between institutions and individuals is enormous. Other industries watched. Other unions took notes.

The SAG-AFTRA strike was not the end of the AI fight in Hollywood. It was the first time the fight had terms.

The Foundation Nobody Paid For

Underneath every AI creativity tool, beneath the elegant interface and the impressive demo and the investor deck showing the growth curve, is a dataset. And underneath most of those datasets is a question that has been actively avoided rather than honestly answered: who consented to this?

AI image generation systems were trained on billions of images scraped from the internet without the knowledge or permission of the people who made them. AI writing tools were trained on vast archives of text — books, articles, essays, journalism, creative work — produced by people who received no compensation and in most cases no notification. AI music tools absorbed decades of recorded music, and the musicians whose sonic signatures are now reproducible on demand were not consulted about whether this was acceptable.

The legal challenges are real and ongoing. A coalition of artists sued Stability AI, Midjourney, and DeviantArt, arguing that training on their work constitutes copyright infringement. Getty Images sued Stability AI. The New York Times sued OpenAI and Microsoft over the use of its journalism. These cases are moving through courts that are being asked to determine, without clear precedent, whether ingesting creative work to train a commercial AI system is fair use or theft.

Whatever the courts ultimately decide, the underlying economic fact is not in dispute: the companies that built these tools extracted value from work that artists, writers, musicians, and photographers spent their careers producing. They built profitable businesses on that foundation. And the people whose work formed that foundation received nothing — and are now, in many cases, competing commercially with systems trained on their own output.

The AI companies’ standard counterargument is that training on data resembles how humans learn — that a painter who studies thousands of artworks does not pay licensing fees to every artist whose work she absorbs. There is genuine substance to this parallel. Human creativity has always developed through exposure and absorption. This is not a cynical observation. It is simply how influence works.

But the analogy does not survive contact with scale. A human painter absorbs influences over years and produces a finite body of work shaped, but never replicating, those influences. An AI system processes millions of works in days and can reproduce any artist’s style, on demand, for any paying subscriber, indefinitely. The scope is different. The speed is different. The commercial application is different. The character of what is happening is different, even if the surface description — learning from existing work — sounds the same. And the illustrator who spent fifteen years developing a visual voice that was distinctly hers is now competing with a subscription service that learned from that voice and charges twenty dollars a month to deploy it.

The Adobe Mirror

Adobe is the most instructive case study in the business of AI creativity, not because it is the worst actor in the story but because it sits at the precise intersection where every tension becomes visible.

Adobe built the infrastructure of professional creative work. Photoshop, Illustrator, InDesign, Premiere — these are not optional software choices. For most creative professionals, they are the environment in which creative work happens. When Adobe integrated AI into Creative Cloud, it was not an outside company disrupting an industry it had no prior relationship with. It was the company that creative professionals already depended on, had built their workflows around, and paid recurring subscription fees to access — now offering AI capabilities built in part on creative work produced with its own tools.

Adobe has been careful to distinguish itself from competitors on the training data question. Firefly, its image generation model, was trained on licensed content, Adobe Stock images, and public domain works rather than scraped from the open internet. This matters. It represents a more ethically considered approach than training on whatever data was accessible and litigating the consequences afterward.

But it does not fully resolve the structural tension it is meant to address. Adobe Stock is a marketplace where photographers and illustrators license their work for commercial use. Many of those contributors did not anticipate that their images would be used to train an AI system that would then generate alternatives to their own work. The terms of service may have technically permitted it. The consent was implicit rather than informed — which, in contexts involving significant economic consequences, is a meaningful distinction.

The photographers and illustrators whose work trained Firefly are now watching AI-generated images undercut their stock photography income. Adobe’s quarterly revenue is $5.87 billion. These are not coincidental facts. They are the same transaction described from two different positions in the value chain. The company at the center of the creative professional ecosystem used the creative output of that ecosystem to build a capability that now competes commercially with the people who generated the training data.

This is not a conspiracy. It is a business model. And Adobe is not unique in it. It is simply the clearest example because the relationship between the company and the affected creative professionals is so direct and so long-standing.

How the Value Flows

State the business model plainly, because the rhetoric around AI creativity tends to obscure it.

Companies that build AI creativity tools extract value from creative labor at two distinct points. First, when creative workers produce the work that trains the AI systems, whether or not those workers know their work is being used this way. Second, when creative workers purchase subscriptions to the AI tools built on their output, because the tools are now integrated into the professional workflows they cannot opt out of without losing access to industry-standard software.

The creative worker is simultaneously the raw material and the customer. Her accumulated skills and output train the system. She pays monthly to access the system. The system competes with her commercially. The price the market will pay for her work declines as the system becomes more capable. The company’s revenue grows.

This is not accidental. It is structurally built into the economics of AI development, which requires enormous amounts of high-quality training data and then recaptures the cost of acquiring that data by selling access to the capabilities it enabled. The people who provided the data are not compensated for providing it. The people who are replaced by the resulting system are not compensated for the replacement. The value flows upward, to the investors and the platforms, and the costs are distributed outward, to the workers and the industry.

The companies doing this are not cartoonishly evil. Many of them employ people who think seriously about these questions and are genuinely trying to navigate them responsibly. But responsible navigation is not the same as equitable distribution. And the structural incentives are clear: the more creative labor that trains the systems, the more capable the systems become, the more the systems can replace the creative labor, the more the companies profit. Responsibility, in this context, is fighting against the direction the incentives point.

Three Fights That Will Define the Decade

The business of AI creativity is not settled. It is contested across three fronts simultaneously, and the outcomes will determine whether the restructuring currently underway produces something resembling a fair distribution of value or simply consolidates the gains at the top.

The first fight is over training data. The lawsuits filed by artists, writers, photographers, and news organizations are establishing legal frameworks for whether AI companies can train on creative work without consent and compensation. A loss for the AI companies in these cases would force a renegotiation of the entire economic foundation of the industry. A win would ratify the current model — extraction without compensation — as legally permissible. The courts are moving slowly, as they always do, but they are moving.

Early signs of a licensing market emerging suggest that at least some AI companies anticipate unfavorable legal outcomes and are getting ahead of them. The Associated Press reached a licensing agreement with OpenAI for its news archive. Getty Images reached a settlement with Stability AI. These are not acts of generosity. They are risk management, and the fact that they are happening suggests the companies involved believe the legal foundation of the scrape-first model may not hold.

The second fight is over labor contracts. The Hollywood strike demonstrated that AI provisions can be negotiated into collective agreements and that those provisions can have meaningful teeth. The question for the broader creative economy is whether workers in sectors without Hollywood’s union infrastructure — the freelance illustrators, the independent musicians, the commercial photographers, the graphic designers working without institutional affiliation — can develop collective mechanisms for negotiating their terms. Individual negotiation with AI companies is not a viable strategy. The power differential is too large. Collective action is the only mechanism that has historically worked in situations where institutional power and individual workers are on opposite sides of a technology-driven restructuring.

The third fight is over regulation. The U.S., EU, and UK are all developing frameworks for AI governance, and the provisions affecting creative workers — mandatory disclosure of AI use in commercial content, consent requirements for training data, compensation mechanisms for workers displaced by AI systems — are actively contested in legislative and regulatory processes. The companies with the most to lose from strong regulation are spending accordingly on lobbying. The creative workers with the most at stake from weak regulation are less well organized and less well funded. This asymmetry is not new. It is the standard dynamic of technology-driven labor disruption, and it tends to resolve in favor of the better-resourced side unless there is sustained political pressure to counteract it.

What To Do With This

The business of AI creativity is not something happening to other people in other industries. If you write, design, illustrate, photograph, compose, or produce anything that exists digitally, the market for your work is being restructured right now. The restructuring is happening whether you engage with it or not.

The people navigating this most effectively are not the ones refusing to engage with AI tools, nor the ones who have handed their creative process wholesale to those tools and called it adaptation. They are the ones who understand precisely what they bring that AI cannot replicate — the judgment, the vision, the accumulated specificity of a particular life pressing against a particular form — and who are directing AI toward doing the mechanical work faster so they can spend more time on the parts that still require a human being who has something at stake.

That is a real strategy. It works for some people in some fields. It is not, however, a solution to the structural problem, and mistaking it for one is a way of opting out of the larger contest. The individual who successfully repositions her practice to command premium rates for AI-augmented creative work has navigated the moment well. She has not addressed the fact that the people who were not able to reposition quickly enough lost their livelihoods, and that the economic value extracted from their years of creative work went to the companies whose systems displaced them.

The business of AI creativity is generating enormous value. The question of who captures that value is still being fought — in courtrooms, in contract negotiations, in legislative hearings, in the daily operational decisions of companies that are right now choosing between paying for creative work and automating it.

That fight is not over. It is, in most respects, just beginning. And the people who understand its mechanics clearly — who can see the flow of value, identify the leverage points, and engage with the contest on its actual terms — are better positioned to influence the outcome than the people still waiting for someone to reassure them that it will all work out fine.

It might. But not automatically. And not without the people most affected paying close attention.

This is the third piece in an ongoing series on AI and creativity. The first examined what AI threatens to take from creative work and why it matters. The second explored the genuine possibilities AI opens for makers and builders. This one looks at where the money actually goes. All three are on the page if you want to read them together.

Sources & Further Reading

Brookings Institution — “Is Generative AI a Job Killer? Evidence from the Freelance Market” (Hui et al., 2024) The most rigorous available empirical analysis of AI’s labor impact on creative freelancers. Found a 2% decline in contract volume and 5% earnings drop among freelancers in AI-exposed occupations, with the effects most pronounced among experienced, higher-priced practitioners. Dispels the comfortable assumption that disruption only hits the lowest-skilled workers. → brookings.edu/articles/is-generative-ai-a-job-killer-evidence-from-the-freelance-market

Association of Illustrators — AI Impact Survey (2024) Survey of nearly 7,000 illustrators finding one in three had already lost work to AI, at an average income loss of $12,500. The most direct available data on what displacement looks like at the level of individual creative workers rather than aggregate market statistics.

Stanford HAI 2025 AI Index Report Generative AI attracted $33.9 billion in global private investment in 2024. Organizational AI adoption jumped from 55% to 78% in a single year. The essential contextual scale data without which individual industry stories make less sense than they should. → hai.stanford.edu/ai-index/2025-ai-index-report

Center for Democracy and Technology — “The SAG-AFTRA Strike Is Over, But the AI Fight in Hollywood Is Just Beginning” (2024) The clearest-eyed legal analysis of what the 2023 SAG-AFTRA contract actually achieved on AI provisions and, more importantly, what it deliberately left unresolved. Essential for understanding the gap between the political narrative of the strike’s success and the actual enforceability and completeness of its terms. → cdt.org/insights/the-sag-aftra-strike-is-over-but-the-ai-fight-in-hollywood-is-just-beginning

AI Creativity and Art Generation Market Report (Market.us, 2024) Market sizing and growth trajectory: $13.5 billion in 2024, projected $141.7 billion by 2034 at a 26.5% compound annual growth rate. Advertising and marketing account for 30.7% of current revenue. The numbers that explain why the business incentives are what they are. → market.us/report/ai-creativity-and-art-generation-market

Adobe Q2 2025 Earnings Report Record revenue of $5.87 billion, 11% year-over-year growth, $125 million in AI-specific annual recurring revenue from Firefly and related tools. The clearest single-company data point on what AI creativity is worth to the platforms that distribute it. → Available via Adobe Investor Relations at adobe.com